Compliance vs. Competitiveness in Costing Methods

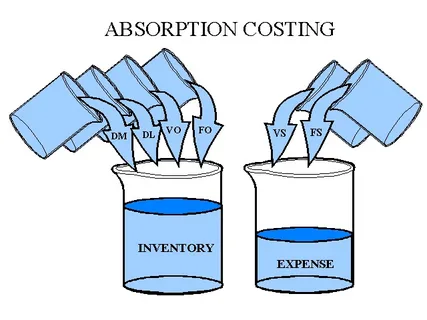

Absorption: All manufacturing costs (fixed and variable) are absorbed into products, offering simplicity but less precision.

ABC: Costs are traced to activities, then allocated to products based on cost drivers, improving accuracy and insight.

Together, these approaches represent the tension between compliance and competitiveness.

Key Features

Absorption Costing

- Spreads fixed overheads evenly across units.

- Simple and approved under IFRS/GAAP.

- Best suited for mass production environments.

Activity-Based Costing (ABC)

- Allocates overheads based on activity cost drivers.

- Produces more accurate, detailed cost insights.

- Better for diverse, service-based, or complex product lines.

Formula Comparison

Absorption Costing Formula:

Unit Cost = DM + DL + Variable OH + (Fixed OH ÷ Units Produced)

Example: Cost per unit = 355

Activity-Based Costing Formula:

Unit Cost = DM + DL + (Activity Overhead ÷ Activity Driver Units) × Activity Usage

Example: Cost per unit = 850

ABC highlights resource consumption more accurately, especially in multi-product environments.

Statistical Comparison

- Adoption: Absorption (65%) vs. ABC (35%).

- Accuracy: Absorption ±15% vs. ABC ±5%.

- ROI: Absorption ensures compliance; ABC delivers ROI in 2–3 years.

- Implementation Costs: Absorption = low 💵 vs. ABC = high 💰💰💰.

Industry Use Cases

- 🏭 Automotive → Absorption.

- 🏥 Healthcare → ABC.

- 🛍 FMCG → Hybrid.

- 💻 IT/Consulting → ABC.

Case Study: Hewlett-Packard (HP) Transition from Absorption to ABC

Background (1995 – Absorption Costing):

In the mid-1990s, Hewlett-Packard (HP) relied on absorption costing in its printer division. While compliant, the system masked the true cost of supporting low-volume customized printers. Overheads were spread evenly, leading to overproduction of low-margin models and underpricing of resource-intensive variants.

- 1995 Results under Absorption:

- Reported Gross Margin: 18%

- Overhead Variance: ±14%

- Strategic Decisions: Volume focus, weak visibility into support costs

Transition to ABC (1997):

By 1997, HP adopted ABC to trace costs to activities such as order processing, technical support, and warranty claims. Cost drivers aligned with actual resource use, giving managers better product-level profitability insights.

- 1997 Results under ABC:

- Reported Gross Margin: 23% (↑ 5%)

- Overhead Variance: ±4% (↑ accuracy)

- Strategic Decisions: Reduced unprofitable models, reinvested in high-demand lines

Impact:

The transition revealed that nearly 30% of products previously “profitable” were eroding margins. With ABC, HP improved pricing, cut hidden costs, and strengthened long-term profitability.

Margin & ROI Impact

- Absorption: Stable-looking margins, but risks of overproduction and hidden losses.

- ABC: Real margins revealed; enabled identification of unprofitable segments and growth opportunities.

Decision-Making Impact

- Absorption: Ensures compliance, but may distort decisions due to inaccurate costing.

- ABC: Provides strategic insights, improves pricing, identifies cost inefficiencies, and supports competitiveness.

Conclusion

- Absorption = Compliance 📑

- ABC = Competitiveness 🚀